Author: Nicholas Dimmock BA MBA(CASS), Director of Investor Relations, 350 PPM Ltd.

_____________________

Headlines

Storelectric: new investment round with 350 PPM open; applies for significant grant from the EU.

Solar 350: receives indicative offer for debt on 1st 30 MW solar project and is now close to selecting equity partner for 420 MW pipeline.

350 PPM: launches Storelectric expansion capital raise and Santander UK 7.375% Bond.

_____________________

About 350 PPM

350 PPM Ltd is a corporate finance house, providing green investment opportunities (and structuring tax incentives where possible) to UK and International Investors and assisting “green” companies to raise finance and develop their businesses:

350 PPM Ltd identifies Companies, Projects and Technologies that it believes will benefit substantially from the implementation of The Paris Agreement; the new global treaty to combat climate change, which has been ratified and comes into force on 1st January 2020.

350 PPM then structures these opportunities under the UK’s Enterprise Investment Scheme (EIS) if possible and works with, advises and raises finance for the above businesses along the commercialisation runway, to ensure they reach their full potential.

The commercialisation runway is defined within 350 as 4 financing stages: Incubation, Expansion, Venture Capital, and Listing via 350’s NOMAD Partners.

350 PPM always invests in the companies it champions alongside its investment clients. By working closely with the company at every stage and assisting in its growth where possible, 350 PPM can protect its and its investor’s interests, influence the outcomes and share in the company’s and its clients’ success both now and in the future.

All companies that 350 PPM champions are designed to profit extensively from the implementation of The Paris Agreement. The Paris Agreement is expected to increase environmental investment by circa 1 trillion USD per year above the existing base case each year on average between 2016 and 2050. (Source: International Energy Agency: http://www.iea.org/Textbase/npsum/ETP2012SUM.pdf )

Sir Nicholas Stern, estimates that not combating climate change will lead to losses in global GDP of between 5 and 20% based on several factors the most significant of which are breakdowns in supply chains, global unrest through loss of agricultural capabilities, fresh water supply issues, loss of land mass and housing.

Summary and Link to Actual Report can be found here: https://en.wikipedia.org/wiki/Stern_Review.

_____________________

Table of Contents

Executive Summary & Economic Commentary

_____________________

Executive Summary & Economic Commentary

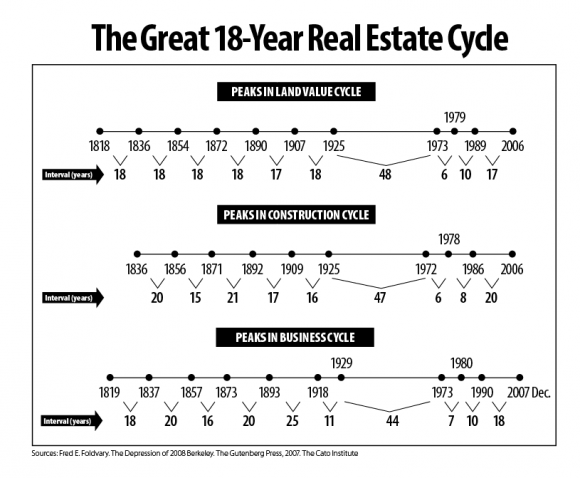

Economically, we are probably now at the end of the of the mid cycle slowdown / correction. That’s if you subscribe to the simple behavioural finance related, “4-year recession and then two 7-year expansive periods (1st is recovery, second is expansion) with a hiccup in between” theory.

The hiccup is 2018, and now we should enter the expansion phase.

This is actually the Land / Housing Economic Cycle, but as land / housing prices fuel everything as a base for major decisions it’s probably not a bad system to follow. It certainly avoids the noise of other smaller economic themes which are very difficult to quantify.

I have written about it before here and there is lots of information on the internet.

Here’s an update in simple graphical form:

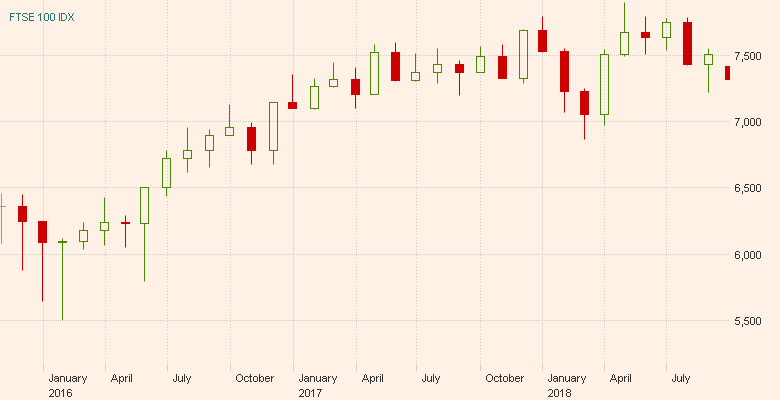

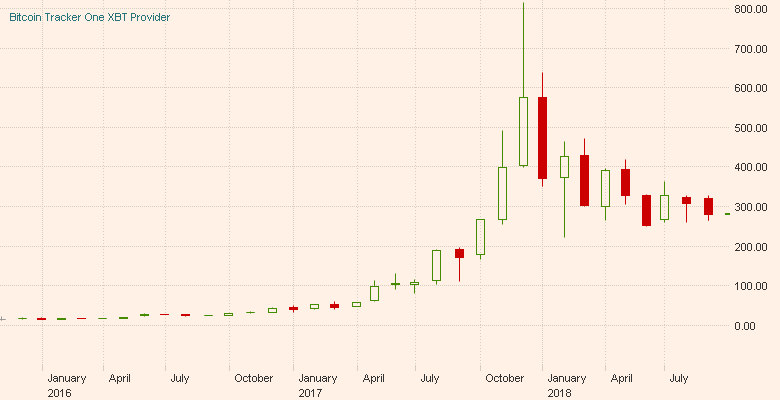

Generally, the mid cycle hiccup takes aim at assets that have grown the fastest and where investor sentiment and confidence levels are vulnerable. This year’s hiccup took aim at bitcoin and of course affected the major indices as well.

Here’s a chart of the FTSE 100 – we clearly have been going nowhere since January 2018:

Here’s a chart of the Bitcoin Tracker One XBT which replicates Bitcoin. Obviously, it takes quite a hit from January 2018.

The 2nd 7 year expansion phase should run up to 2023.

Environmental Economics

Of course, unloved, beaten down assets do not seem to take much notice of these macro themes.

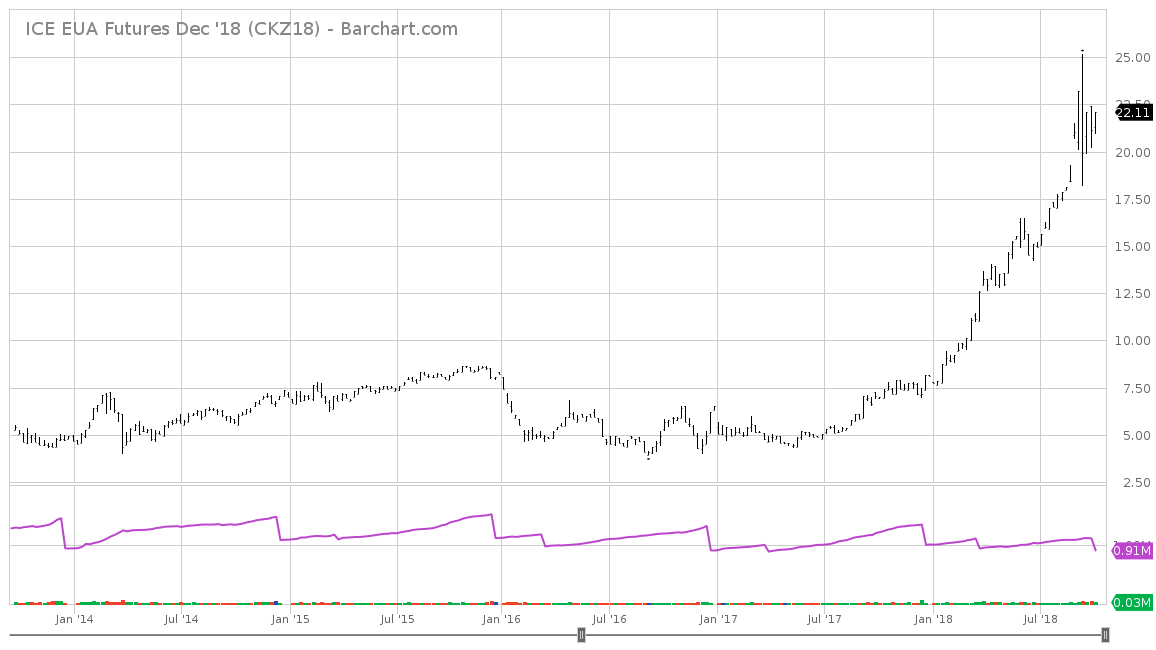

From an Environmental Capitalist point of view, The European Union Allowance, which is effectively a permit that allows organisations to pollute the atmosphere, acts as a good proxy for the health of the environmental revolution.

An effective EUA price short term is probably around €60, though I can see it going to €120 as The Paris Agreement starts to bite and climatic conditions get worse which they will do quickly.

This is the 5 Year EUA Price Chart:

The Conference of The Parties To UNFCCC

(The United Nations Framework Convention on Climate Change)

COP 24 is due in Katowice, Poland. There is a considerable agenda for sovereign representatives and Heads of State during the 2 week meeting.

We will cover what happens in the Winter Update, but here is some initial information:

Details of COP 24 can be found here: http://cop24.gov.pl/en/

Full Google Search on COP 24: https://www.google.co.uk/search?q=cop+24&oq=cop+24&aqs=chrome.0.69i59l2j69i60l3j0.2840j1j7&sourceid=chrome&ie=UTF-8

350 PPM Ltd

I think that the last thing that 350 PPM can be accused of is of being a high-volume low-quality provider of Environmental Investment Opportunities. We have now been trading for 18 months and have offered 3 such opportunities to our investor base. This is against companies that offer 10 opportunities every month.

We select companies, market them, advise them, work with them, promote them to our network of high net worth, venture capital / private equity investors as well as industry investors and counter-parties that may wish to partner with them on certain ventures. In due course, we will introduce them to appropriate NOMADs to assist them to list their businesses on an appropriate exchange.

If they do well after the “incubation” stage of financing we provide, we will beckon them back for a further round of financing; our “expansion” stage. Doing well means achieving the milestones we have agreed with the companies or other suitable positive developments within their businesses, accessing the tax reliefs (if applicable) they claimed to be due, and increases in their share price commensurate with their increasingly positive prospects.

If not, they are on their own: either they fight or die. But if they do fight and progress, they come out stronger having cut the fat from their organisation and due to their concentration on earning money as opposed to raising it. Of course, every early stage company needs additional capital to expand in the competitive marketplace but being constantly reliant on raising outside funding is negative and utilises resources that could be used to gain revenue and in due course profits.

Solar 350 is an excellent example of how this should work. It’s had no funding since September 2017 yet has made huge progress.

______

During PPM’s first year of trading, we have hired and subsequently parted company with several Investor Relations Consultants. You can’t hire the best as a start-up, so this turnover is natural.

Our current team of Investor Relations Consultants; Chris, Paul and Lexi, is exceptional: pragmatic, intelligent, hardworking, with complete belief in the investment theme that we are following, a keenness to acquire shares themselves in our corporate clients, a focus that is at least 70% “Jam” tomorrow and following our principles of putting our investors first, the company (350 PPM) second and placing themselves in third position.

This doctrine is out of the Peter Hargreaves, “In for A Penny” Autobiography / Business Adventure. For those of your not familiar with Hargreaves Lansdown; this mail order, research led stockbroker was started from a back bedroom in the 80’s and is now worth £10.17 Billion.

You can find the book here on Kindle, just in case you’d like to read it: https://www.amazon.co.uk/dp/B002SCQG56/ref=dp-kindle-redirect?_encoding=UTF8&btkr=1

(just by the by: Black Edge of which “Billions” with Damien Lewis is based on, is also excellent – effectively the story of how cheating became legal and “A Colossal Failure of Common Sense: The Incredible Story of the Collapse of Lehman Brothers” is mind-blowing – effectively the story of how employees (bankers and mortgage salespeople alike) rip apart economies and businesses for personal, short term gain). My personal favourite is The Greatest Trade Ever, John Paulsen’s story of swimming against the housing market from 2001, and making $20B in 2010 and 2011.

You can find them here just in case you fancy a read:

(Nominated for the FT/McKinsey Business Book of the Year

Nominated for the Carnegie Medal for Excellence in Nonfiction

Amazon Top 5 Business Books of 2017)

https://www.amazon.co.uk/dp/B0035X1BSO/ref=dp-kindle-redirect?_encoding=UTF8&btkr=1

So, What Is My Point?

My point is that if the companies hit their targets, they can come back from another round of funding. If they don’t hit their targets, strive and achieve, we stop funding them and they are on their own.

If investors choose to invest in companies we have once funded and decided not to anymore, through investor relations staff we once employed and decided not to anymore, I am sorry, but you are on your own in regard to the specific transaction you are undertaking.

Moving Forward

One company that has hit, surpassed and effectively smashed their milestone targets with PPM is Storelectric Ltd.

It is difficult to find a more substantial opportunity of its time: chiefly, as the paradigm shift to cleaner power generation gains further traction and is reinforced by International Treaty (The Paris Agreement), Storelectric has the team, technology, competence and capability to facilitate the shift.

Very simply, due to intermittency issues with renewables, grids cannot generally push past 15% Renewables / Fossil Fuels without substantial and expensive emergency and fast response electricity generation – typically gas turbines at very high prices per MWh. The global targets under The Paris Agreement require 85% energy generation from renewables by 2050.

Energy storage is an alternative solution to fast response fossil fuel generation, yet batteries are expensive, low power, low energy capacity, short duration of discharge and do not scale well with size (amongst other issues).

Storelectric’ s solution is to compress air in sealed underground chambers during a compression cycle when electricity prices are cheap or negative (when its windy for instance) and to run the decompression cycle (letting air, compressed to up to ~70 bar out through a turbine, which turns a generator thus generating electricity) when prices are high. FYI: UK 1-hour-ahead electricity prices recorded minimums of -£27 GBP per MWh and maximums of over £1,000 per MWh in the UK in 2017.

Energy storage has long been seen as critical in the large-scale deployment of renewables and as Storelectric’ s solution is proven, improved, patent pending, highly scalable to 1GW+ per site and inexpensive, they have our full backing.

Accordingly, we are now raising for Storelectric’ s planned Crowdfunding raise. It is the success of this pre-crowdfunding raise that PPM is involved in, that will act as a catalyst for the crowdfunding raise – as a rule of thumb, if this is structured correctly, which we believe it is, every £10k PPM and its counter-parties raise will be matched with a further 10 to 30K on the electronic platform.

Which means we can get scale into our raise and Storelectric can achieve their funding goals more quickly.

Now onto the reports…

_____________________

Solar 350 Ltd

Starting Price: £2.50 per share

Current Price: £30 per share

———-

Following on from our last update when Solar 350 had signed an agreement with PAPA ONE Ltd (Paris Agreement Project Accelerator), we received the first down payment for circa $70,000, after which PAPA ONE’s main backer experienced a very significant loss, rumoured to be around £12M on a Film Investment.

Obviously, we are going to keep hold of the $70,000, (although we might convert this into shares in the project company for him due to his unfortunate circumstance) but in the interim, we have launched an Auction to find an equity investor for all the sites (yet only approaching well capitalised entities with existing operations within the Solar industry on this occasion).

The bids are due in on the 21st of October.

Also, during this period, we have been in contact with a number of the lending banks in Mexico and have now received an indicative offer for circa 60% of the project costs as detailed below:

Dear Peter,

I hope that you are very well. We just got an indicative quote from our finance area for your project. We are looking at the following:

- Total Term: 240 months

- Disbursements Term: 12 months

- Amortization scheme: every semester

- Structuring fee: 2% + VAT

- Availability Fee: 0.5 + VAT% (over the non-used balance)

- Interest Rate: TIIE 28 days + margin

- Margin: 260 basis points

- The credit will be in Mexican pesos.

As discussed previously, the amount of the credit will be sized over the financial model subject to a series of constraints over debt service coverage ratio indexes.

I hope to hear from you soon.

Obviously, if you have 60-70% of project capex in debt, you need 30-40% equity and then you’re done.

As is, on Friday, we are likely to agree provisional terms with an EPC for a further 20% of funding, which leaves our first project with a 20% funding gap which we will most likely have agreement in place to fill by the end of the month via the auction.

Just on other news, we are now down to a technicality regarding Enterprise Investment Scheme qualification. The specific technicality is our start of trading date, which we assumed would be the date Solar 350 opened its doors to attract business.

This is apparently not so in HMRC’s eyes. They consider the trading start date as the moment in time when a company has a reasonable chance of creating some revenue and being paid.

I have now provided them with a suitable agreement from a landowner in Chile and I am hopeful that they might now honour our EIS Status and consider this the start of our trading date.

Electricity Prices

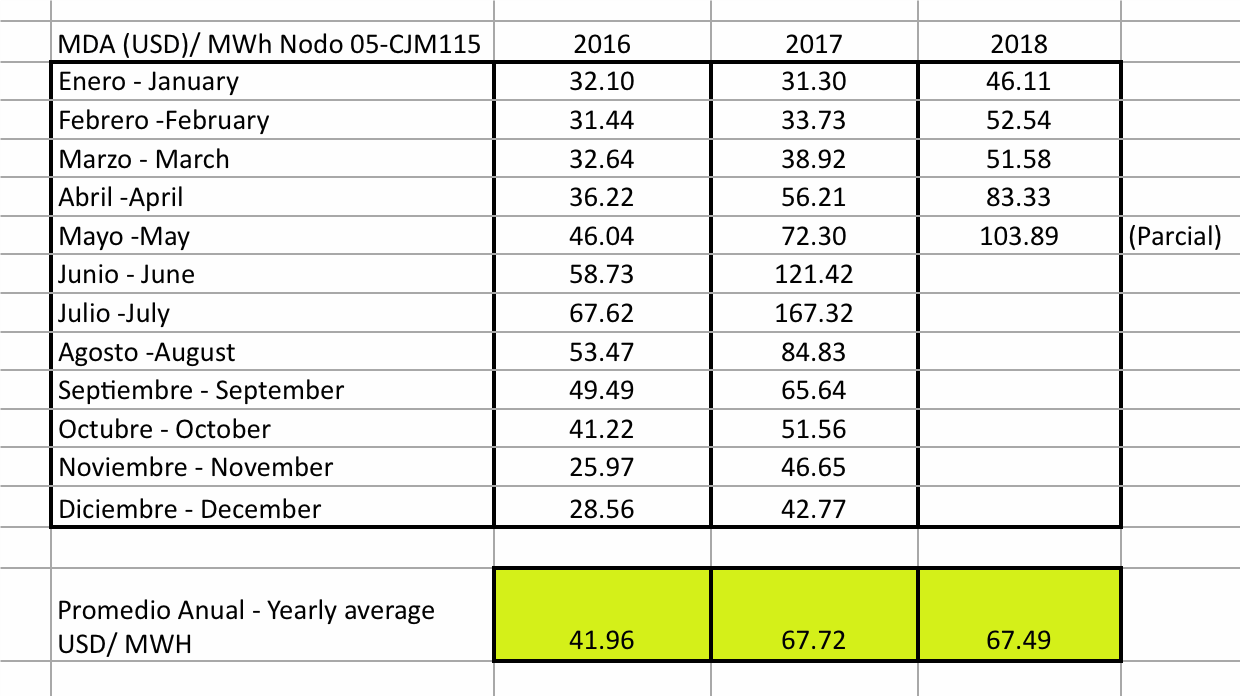

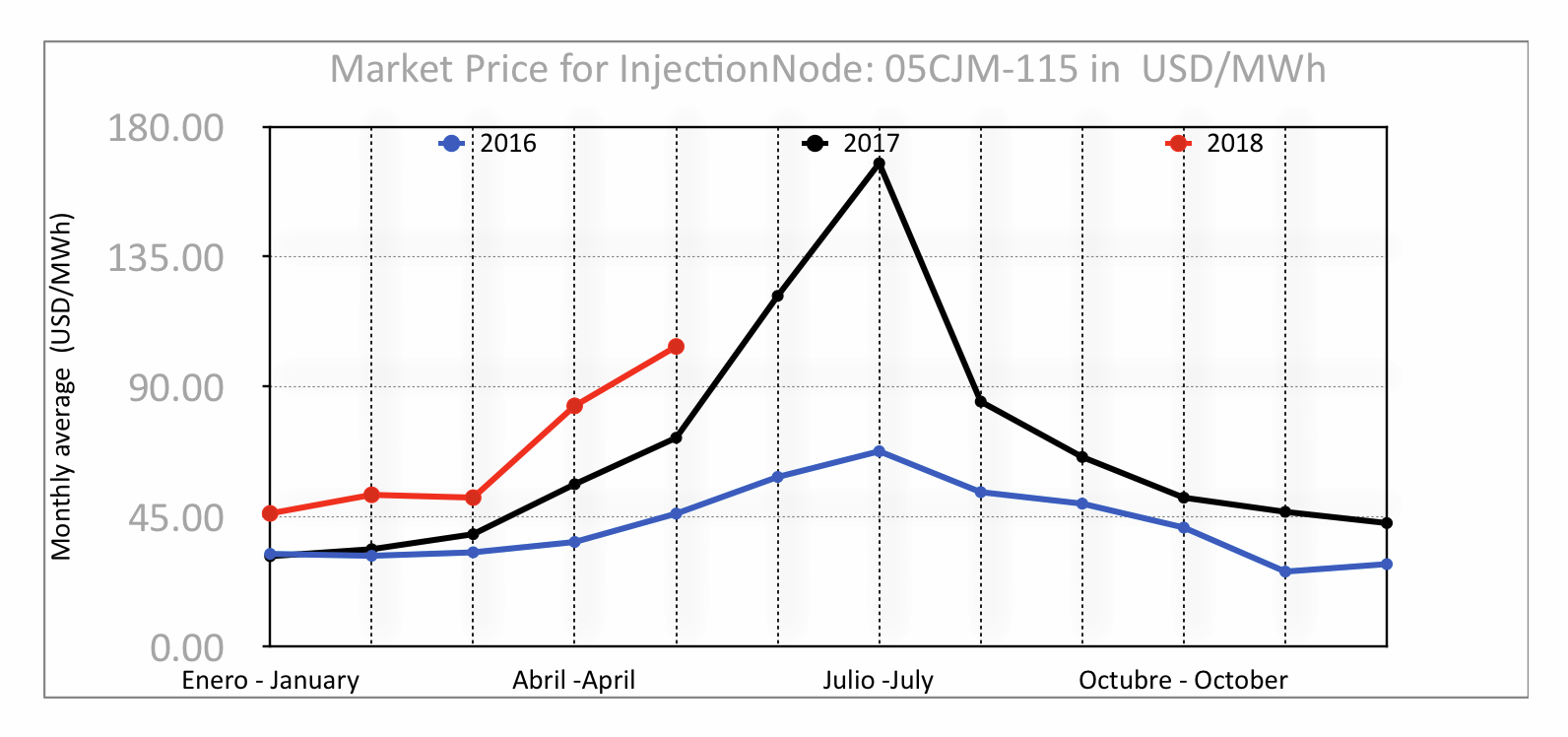

Please see below electricity prices from the node of the 1st Project we are looking to place. Evidently, these are increasing at circa 61% per annum:

May 2018 full figure was $131 USD per MWh. Forecasts for 12 months to Feb 2019, indicate an average of $109 per MWh plus CEL’s (Clean Certificates). CAGR demonstrated at this node is circa 61% per annum. We have modelled $100 and $15 on the CELS (Green Certificates).

Graph of CFE Offtake Pricing on PML on Injection Node: 05CJM-115 for each year (Blue 2016, Black 2017, Red 2018):

For those of you that would like an independent review of what is happening in Mexico and LATAM, please click on the following link or simply Google Search: Mexico Solar, LATAM Solar or similar.

Mexico’s Solar Market Is Booming, but Still Has Key Hurdles to Clear.

Greentech Media: https://www.greentechmedia.com/articles/read/mexicos-solar-market-is-booming-hurdles-clear

The future looks bright for solar energy development in Mexico – pv …

PV Magazine: https://www.pv-magazine.com/2018/02/19/future-looks-bright-for-solar-energy-development-in-mexico/

Will Mexico Be the Next Solar Super Power? | Morgan Stanley

https://www.morganstanley.com/ideas/mexico-decarbonization-solar-power

—

____________

350 PPM LTD

![]()

Starting Price: £12.50 per share

Current Price: £170 per share

———-

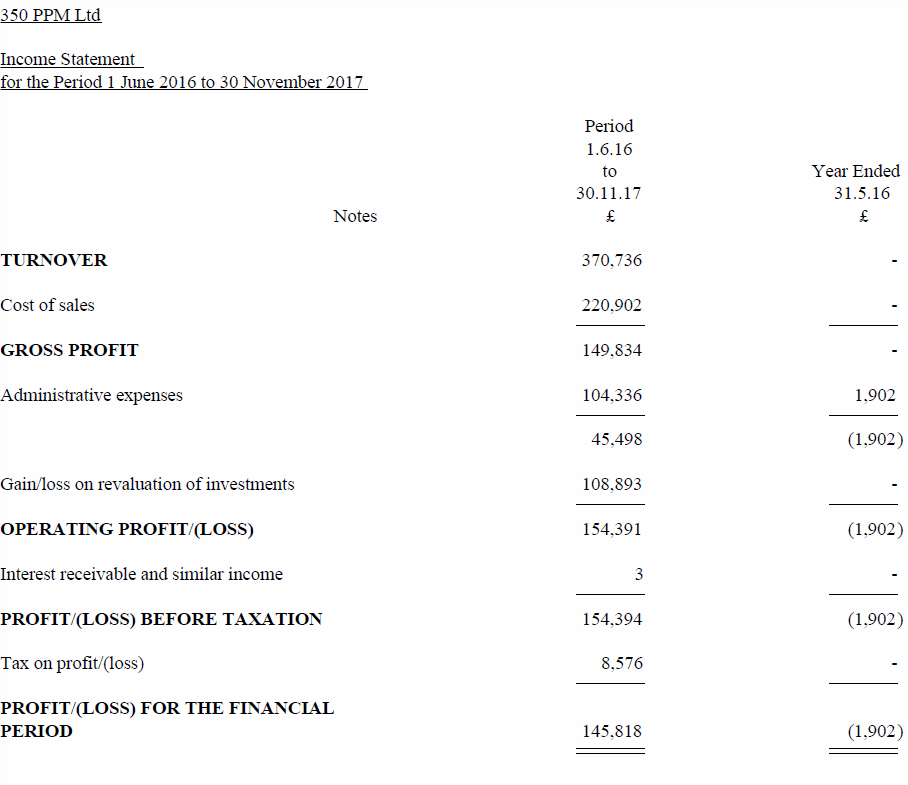

350 PPM Accounts have now been filed.

In short, we recorded a Profit for the financial period of 1st June to 30th November of £145,818. Please bear in mind that we got out FCA Authorisation in August 2016 but did not start trading until January 2017.

The Income Statement is detailed below:

With the improvements we have made through restructuring the business since last year and the new business model we have implemented, which will add additional scale and subject to us being able to source sufficient investment opportunities within our sector this year, we are hopeful that we can increase our turnover 300% in the year November 2018 through to 2019.

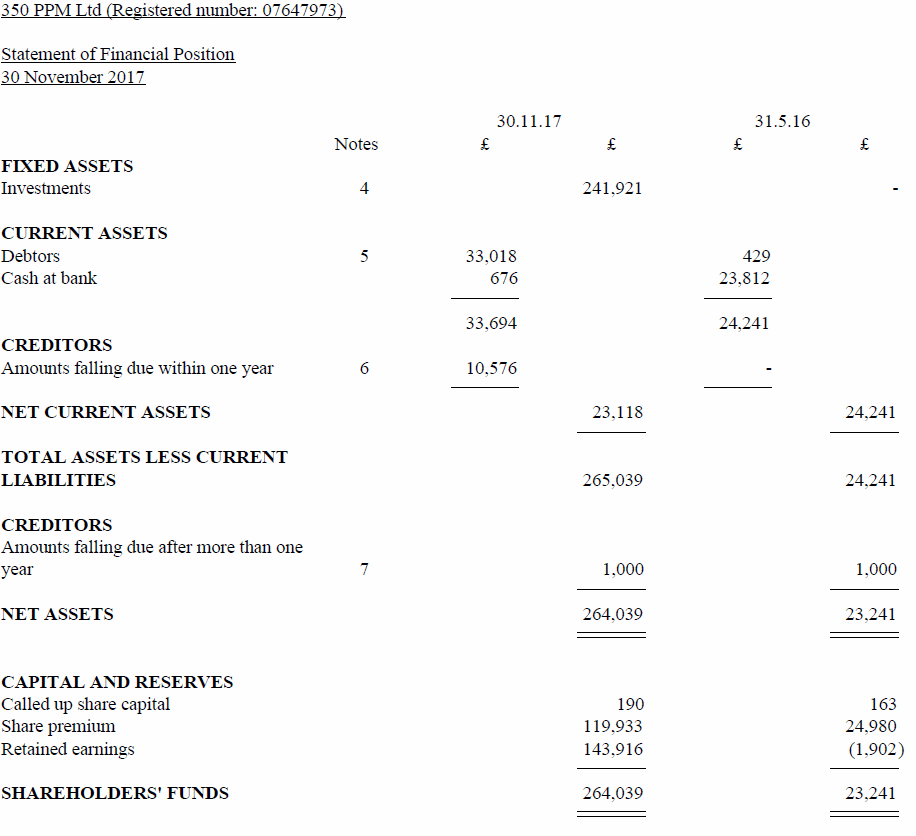

Our financial position from our accounts / aka our balance sheet is detailed below as per our Accounts Submissions to Companies House:

Our balance sheet shows £241,921 which is based on our positions within Solar 350, Disarmco and Storelectric. From memory we priced these in at £13 and £60 per share respectively less likely disposal costs. Both of these now have further to run for our accounts for 17-18. We have however sold out of the Disarmco Shares as we had an offer to exit and could make use of the cash at the time.

While our equity business is again prospering, our fixed income business shows little signs of life. Investors seem obsessed with the dubious nature of the Renewable Energy Bonds issued to companies mostly advertising on Google Adwords. From my investigations these are equity investments dressed up as debt and secured against assets under construction. Many of these, in my opinion have the potential to unwind, as there are significant construction and connection risks which will mean the assets will never generate cash.

None of the brokers offering have any reputation and most are not regulated by the FCA – they are unregulated and promoting regulated investments. If you are not bothered by 2 years in prison and unlimited fine or both, then why are you going to be bothered about an investor doing well.

I am unable to identify quite how they will falter, but I would put a risk rating on this of circa 50%.

This is an example of one that did.

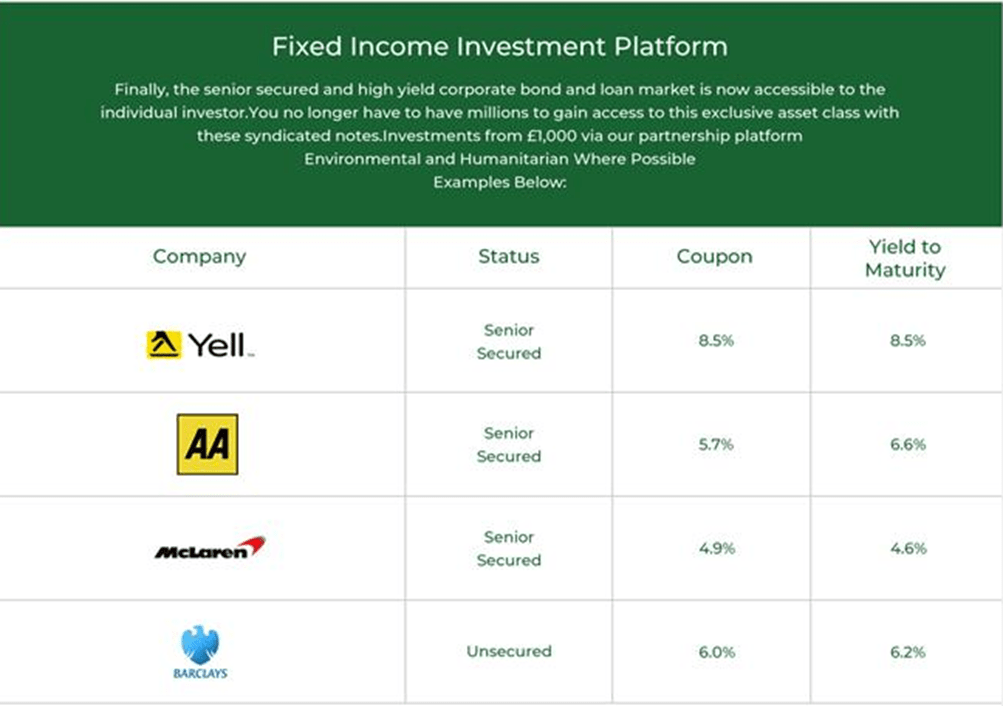

Conversely, our platform offers syndicated bonds from well-known issuers such as Barclays Bank, McLaren, AA and Tesco.

If you choose their hybrid / smart interest product this offers 6% with maturity date of 2023 and invests in all the bonds at one time. You can gain access to the site from here if you’re interested in seeing what is available: https://www.wisealpha.com/350ppm

There is no difference to the products performance in coming through us, we just make a commission if you do.

Some examples are detailed below:

Investor motivations always baffle me. 6 % to lend to Barclays with early exit possible, is in my view outstanding, although the hybrid smart interest paying 6% diversified across circa 40 credit worthy listed issuer would reduce the risk of default from 1-2% on an individual company to circa 0.0375%.

In my opinion only and not providing any advice on a Risk to Reward basis, this product is exceptional. Anyway, you’ll decide for yourself.

In Closing

Just in finishing, we are always looking for new clients. If you have friends, colleagues, (other family members (bit risky I know), rich and powerful enemies, please don’t hesitate to put them in touch with us or at least provide them with our details.

Or they can register here themselves: https://350ppm.co.uk/investments/

Strong global economic expansion should now run naturally to 2023 as part of the established 18-year economic cycle. In addition to this, The Paris Agreement requires investment of 2.5% of global GDP per annum to hit the 2% target from 2018 onward to 2050. Obviously, this increase is not going to happen overnight and most likely will happen in the form of a right skewed bell curve.

Regardless, a 2 trillion USD per year sector increase, in aggregate demand for environmental products, projects and technologies is sufficient demand to launch most competent and capable businesses let alone world beating ones.

Disarmco Holdings Ltd

![]()

Starting Price: £5.51 per share

———-

News is confidential and will be emailed to investors separately.

Storelectric Ltd

![]()

Starting Price: £24.85

Current Price: £150

———-

People new to Storelectric may benefit from reading the last Storelectric update, as it contained significant news not repeated in detail here.

New Investment Round Now Open

As mentioned above, Storelectric is now accepting further investment through 350 PPM. The six-word pitch for Storelectric is ‘enabling renewables to power the world’. This is achieved by storing renewable energy on a large-scale using Compressed Air Energy Storage (CAES). CAES works by using electricity to compress air, then expanding this air through a turbine when needed. As covered in the previous update, Storelectric is now supported by NAM, the largest energy company in Holland, jointly owned by Shell and Exxon. Investment is sought for 2018-19 to screen and progress a pipeline of plants to the point of stand-alone investment readiness, as well as to support business operations and further develop the technology.

To learn more, new investors can register at https://350ppm.co.uk/investments/. Existing clients can contact their 350 PPM representative or contact us.

The initial target is £300,000, which it is planned would be used as a catalyst to kick start a crowdfunding raise on Crowdcube starting in November. Given the progress Storelectric is making – see below – this may well be the last opportunity retail investors have to participate in the near-term.

Please note that we have already had a huge response both from existing Storelectric investors and from new investors as a result of our external marketing efforts. If you are waiting for your transaction to be processed, apologies, and please rest assured that our settlements department (the wonderful Ilona) is diligently working away with the objective of getting up to date by close of business Thursday.

News

NAM (the oil and gas giant that Storelectric won a competition with in July) has sent Storelectric a draft written cooperation agreement, previously verbally agreed at the joint NAM-Storelectric workshop described in the previous update. We hope to share some further good news on this front shortly.

Mark Howitt (CTO) has been working tirelessly with Ernst & Young to prepare the PCI (Project of Common Interest) application, potentially opening up a grant of 50% for an initial study for the 40MW and 500MW Cheshire projects. This application has now been submitted. Storelectric is now the only company that has a large-scale energy storage project (that isn’t pumped hydro) as part of the current Projects of Common Interest in the EU making it eligible for this grant award. Learn more about this – including the UK government EU funding guarantee – at http://www.cares-pci.uk/.

Storelectric has now initiated the pre-planning application for its 40 MW plant in Cheshire, one of the precursors to a ramp up of the FEED (Front End Engineering Design) phase (once completed this will culminate in a shovel ready project with full planning permission). Funding for FEED is included as part of the PCI bid mentioned above.

Tallat Azad (MD) spent the early part of August in Inner Mongolia at the invitation of the President of World Energy Forum. His report, which can be found at this link, includes a short but illuminating interview with a Noble Laureate in Physics (and a Professor of Physics from Stanford University), someone passionate about storage and CAES in particular.

Jeff Draper (FD) has been working with companies interested in exploring CAES & hydrogen storage and this culminated in a symposium (jointly hosted by Storelectric and a sister company Hydrogen Energy Storage Ltd) in August. The symposium was filmed and you can see the interviews conducted during the day that give a flavour of the importance of storage and the prominence of the companies and entities that attended and are interested in the storage field by clicking here.

_____________________

Contact Information

Tel: +44 (0) 203 151 1 350

Fax: 0203 151 9 350

Level 1, Devonshire House, 1 Mayfair Place, London, W1J 8JA, United Kingdom.

_____________________

Risk Warnings

350 PPM Ltd is an Appointed Representative of M J Hudson Advisors Limited (FRN: 692447) which is authorised and regulated by the Financial Conduct Authority in the UK.

The value of your investments and the income from them can fall as well as rise. An investor may not get back the amount of money invested. Past performance and forecasts are not reliable indicators of future results. Currency denominated investments are subject to fluctuations in exchange rates that could have a positive or adverse effect on the value of, and income from, the investment. No representation or warranty is given as to the availability of EIS relief / reliefs. Since the requirements to fall within the EIS must be monitored all the time it is possible that if the requirements are met today, they might not be tomorrow. Investors should consult their professional advisers on the possible tax and other consequences of holding such investments.

The investment opportunities in this website are only available to persons who would be categorised as “professional clients” (including “elective professional clients”) as set out in COBS 3.5 of the

FCA Handbook: www.handbook.fca.org.uk/handbook/COBS/3/5.html. There is no access to the FSCS. Your capital is at risk if you invest. Please see the full Risk Warning here.